Is FranklinCovey The Next ADOBE?!

YUP!

FranklinCovey over the past 7 years has transformed from a products company to a high margin recurring subscription service. ADOBE underwent a similar transformation in the past.

77% of total company revenue is now subscription and continuing growing.

In fiscal 2022 subscription revenue grew 29% and maintained its greater than 90% renewal rate.

Gross margins for the entire company in 2022 were 77% and gross margins on their fast growing all access pass subscription is 85%

All access passes accounts for about 55% of company revenue at this point in time but I believe it accounts for a vast majority of company earnings.

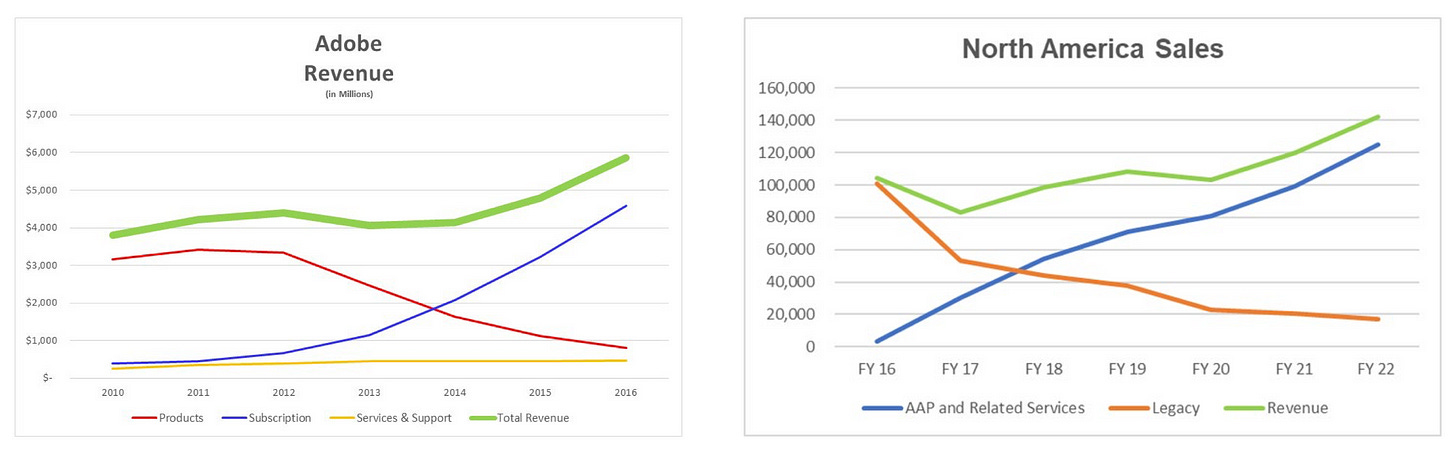

Here is a chart of how the management team is viewing the future of the business:

Management believes that 2016 Adobe is similar to current day FranklinCovey. This chart shows that as legacy product business turns into new subscription business, there is an increase in both revenue and profitability.

When asked about what they plan to do with the new cash flow they’re going to be generating, management responded with : increasing their sales force and buying back stock…These are both answers I like to hear!

With this type of business transformation usually comes a multiple re-rating.

This sort of business has high visibility as it is pretty heavily contract based and they recognize much of their revenue before they perform the service. In addition, management has a history of being conservative in their estimates, so I trust their 2025 projections.

Management believes they’ll produce $67 million in earnings in 2025 meaning the company is trading at 9x 2025 earnings.

This one has a very, very attractive business model, but for me it’s not quite cheap enough yet.

I will be patient, keep an eye on it, and if it gets a little more attractive I think we should scoop it up!